15 Minutes Read

Creating A Winning Business Model

We see many entrepreneurs come to us with brilliant ideas an inventions, but the business model is lacking in some…

Last Updated: 1/7/2022

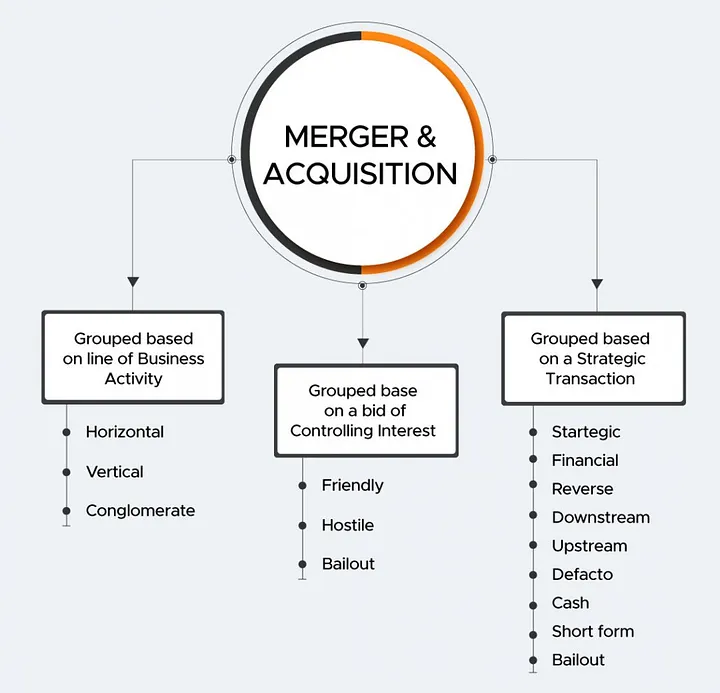

Mergers and Acquisitions (M&A) are often used together, although they mean different things. Both words are used to explain the joining of two companies or businesses. This joining process could be through different forms of transactions. These transactions could be: either a merger, acquisition, consolidation, purchase of assets, management acquisition, or even a hostile takeover. All these terms have different meanings and imply a lot of different processes and management rights.

If a company buys ownership rights over another and becomes the new owner due to the control of running the business, this will be known as an acquisition. The company has bought or acquired another company to run.

If two businesses that have similar plans for expanding or similar target market and business offerings decide that they should work together as a new entity, this is a merger. The businesses merge their operations. This is usually done to achieve economies of scale. This was widely seen in the pharmaceutical and automotive industries. Many of these listed companies recalled their shares and new shares of the merged companies were issued.

A sale transaction is also called a merger. This occurs when the management of a company decides to sell their shares or business assets to the highest offer. The company being sold is absorbed into the buying company and its operations are absorbed (or merged) into the acquiring company. Many new businesses launched by entrepreneurs are acquired in this way by larger companies.

The more dramatic hostile takeover deals are also considered to be acquisitions. As the name denotes, the company being bought is not looking for a buyer

While the entire process of acquiring another business is a complicated one, the most crucial part is the structure of the acquisition. This requires considering a lot of factors like corporate law, legislation about stocks purchase, tax rules, accounting treatment, trust and competition laws, market forces, financing restrictions or debt rules. This determines how attractive the company remains for the buyer.

Some key documents in a merger or acquisition deal are the Term Sheet (which is used as a framework for the entire deal) and a Letter of Intent (LOI) which specifies the broad terms of the proposed deal. A term sheet documents all the details of a deal. It is a brief of the entire deal and sums up the entire contract’s key points. The Letter of Intent is a summary of the transaction to take place. It summarizes the main aspects to be covered in a term sheet and documents whatever is agreed upon by the parties to a transaction.

A key reason to opt for a merger or an acquisition is to achieve economies of scale or otherwise fulfill its growth prospects by expanding into new markets, acquiring new product lines, or simply increasing their bottom line. Going for a merger also helps companies to acquire their competitors. This then allows companies to focus on business growth, instead of competing with their rivals.

While competition is good for innovation, businesses must innovate and try to reduce their expenses at the same time. Acquiring their competition allows them to focus on innovation and worry less about the costs.

Many businesses acquire new companies to add new business strength to their existing lines of business. By going for acquisition, such businesses end up getting an up and running business line that will add variety to their existing business portfolio.

A merger or acquisition allows the buying company to increase its portfolio through the addition of new business lines, industrial patents, human resources, and clientele.

Many companies acquire businesses that offer them options of vertical or horizontal integration along their supply chain. The option of expanding business reach through acquiring businesses up or down their value chain tends to add in a competitive advantage to the business. This combination of business activities also improves productivity and helps to reduce costs of doing business as business synergies start to take effect.

In most cases, the businesses being merged or acquired are usually willing to be absorbed or merged into their buyer. The owners (or shareholders), board of directors, and management are all on board with the merger. In case the shareholders, board or management is not willing to be acquired by the buying company, the acquisition is called a hostile takeover.

Since the company being bought is not agreeable to the acquisition, the company taking over usually must buy up shares of the company from the stock market or from the private shareholders to get a controlling interest in the business

The generic steps involved in different forms of mergers and acquisitions are as follows:

Since mergers are mutually agreed upon combinations of two businesses, the respective boards of directors approve the terms of the merger and seek shareholder approval for the transaction. If the company is (are) unlisted, they inform their stakeholders in private about the terms of the transaction. Any dissent is handled according to the mandate of the ownership and nature of the dissent. In the case of listed companies, their trading symbols are also modified after the merger is completed.

In an acquisition deal, the business acquiring the other business just takes on ownership in the form of a majority holding of its shares. There is often minimal change in both the businesses, and both may continue to operate under their existing trading symbols.

Consolidations

If the acquisition is in the form of consolidation, then the acquiring company will modify the acquired company by merging the existing common structures between itself and the company it acquires. Its structure will also be modified to allow for better consolidation of its business structure.

In consolidations, it is essential to get acceptance from company stockholders. In such mergers, it is usual for the company to issue new shares reflecting the new ownership structure of the company.

Tender offers

A company makes an offer to buy all the issued shares floating in the market of the business it wants to buy. This buying offer would be at a share price less than the market price of the shares. The benefit to the company receiving the offer to sell is that it can make a clean (and profitable) exit from the market it is in.

Acquisition of assets

Somewhat like a tender offer, in this form of acquisition, the buying company buys the assets of another company. the only difference is the form of security being exchanged. Again, the company selling must get approval from its shareholders and stakeholders. This form of acquisition is common in the liquidation of companies that have filed for bankruptcy. It is common for bankrupt companies to be bought off piecemeal by other companies interested in their assets. Inventory, plant and machinery, offices and warehouses are common assets that are easily sold off.

Management Acquisition

Also called a Management Buyout (MBO), in this acquisition employees (usually in senior executive positions) partner with venture capitalists or arrange to finance and get a controlling share in their existing or another company. it has been known for MBOs to take on single divisions of large companies and taking it on as a private business. These acquisitions are usually heavily dependent on debt and need shareholder approval. The most famous example of an MBO is the acquisition of Dell Corporation by Michael Dell, its founder.

Now comes the key aspect of an acquisition. The money to make the transaction work. A company can be acquired through several options. These are cash, shares, debt assumption (the buying company takes on the debt of the company it is buying). In some cases, the acquisition relies on a combination of all these or some of these. It all depends on the buying company and the company being sold.

In the case of smaller companies, the direct acquisition of assets is also possible. In smaller deals, it is also common for one company to acquire all of another company’s assets. For example, Company B buys up all of Company S’s assets. This means that company S only has cash and debt on its books now.

Another way of financing an acquisition is what is called a reverse merger. In a reverse merger, a private company is listed quickly. This is done by the private company buying a listed shell company. this is usually done when the buying company needs to raise funds and issue shares for it. The process of becoming a listed company can be time and resource consuming and a reverse merger allows companies to save time and raise capital quickly.

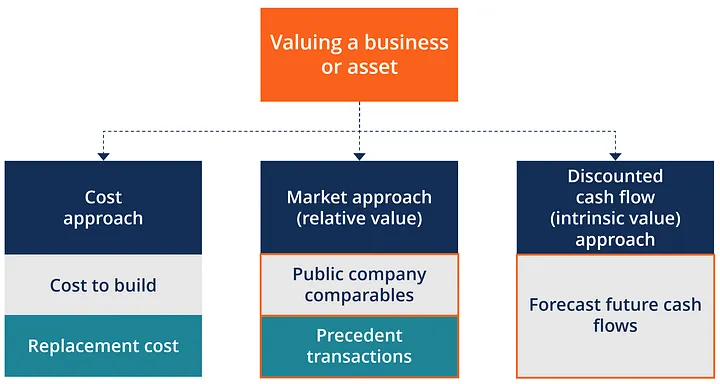

Now that we know how a merger or acquisition can be funded, how does a company decide how much another company is worth? This requires assessing the company and both the company being bought and the company buying will make their valuations of what the merger should be valued at. The selling will try to value as high as possible and the buy will price as low as possible.

The negotiations about the valuation are one of the key flashpoints in an acquisition deal. The use of certain valuation metrics and comparing them with other companies in the industry allows for some objective valuation.

Discounted cash flow (DCF)

A commonly used tool is the discounted cash flow (DCF). The DCF analysis yields the current value of a business based on an estimate of its projected cash flows. Estimated cash flows are evaluated for their present value by applying the weighted average cost of capital (WACC) for the company being bought. The process for working out the discounted cash flows is a difficult one, but it is highly effective.

Price-to-earnings ratio (P/E ratio)

This ratio allows the buying company to make a valuation based on the earnings and market rate of the stock of its target company. Assessing the P/E of all companies in the target company’s group offers a good standard for valuing the company well.

Enterprise-value-to-sales ratio (EV/sales)

This formula allows the company to be assessed about its sales. This formula allows high revenue companies to be valued higher due to higher sales volume. The sales versus its sales price can be compared to other companies in the industry to make the valuation more realistic.

Replacement cost

In some mergers or acquisitions, the worth can be derived based on the costs of replacing the company being bought. For instance, if the value of a company is just the total of its assets and liabilities. The book value method is very crude and oversimplifies the valuation process particularly as it approaches a company from the perspective of its financials alone and does not consider the goodwill and other non-quantifiable and accountable aspects that add value to a business.

Pro Business Plans has been ranked among the top service providers on Wimgo — a company that helps companies get matched with top service providers.